What the Latest Tax Law Changes Could Mean for You (and Why It Matters Now)

Tax law changes tend to fall into one of two categories: the kind that make headlines — and the kind that quietly change your financial life without you realizing it.

Right now, we’re in a moment that’s a bit of both.

In a recent webinar, I walked through some of the most important updates coming out of new federal legislation and what they could mean for your day-to-day financial decisions. And while it’s easy to assume these changes only matter to accountants or business owners, the reality is they touch far more than you might expect.

Here’s what’s worth paying attention to.

The Tax Track

In mid-2025 the One Big Beautiful Bill Act (“OBBBA” for short) passed with sweeping tax impacts to households across America. To understand how it impacts you, let’s first review what I like to call “The Tax Track” that you follow for income taxes.

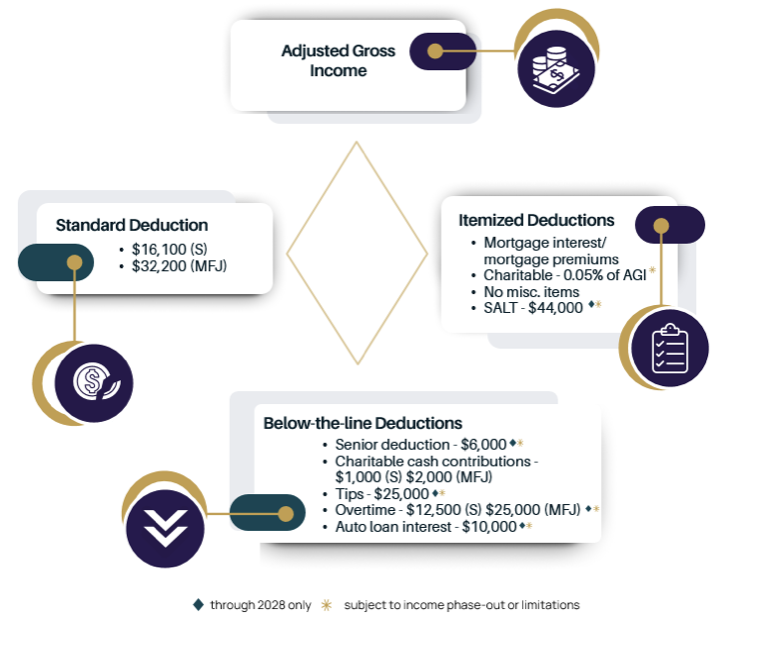

You start with your gross income, which can have some adjustments, and then arrive at your Adjusted Gross Income. For those just filing your taxes, this can be found at the bottom of page 1 on your Form 1040. Your Adjusted Gross Income, or AGI, matters because it is often used for thresholds for certain deductions or benefits when they’re phased out at higher income – or higher AGI – levels.

From your AGI, you then either take 1) the standard deduction or 2) itemize your deductions, typically whichever results in the higher deduction. After that choice, you can have some “below the line” deductions, further reducing the ultimate taxable income. And it’s this taxable income that is then subject to the income tax brackets to calculate your total tax liability.

Yawn… Okay, stick with me. It’s important to know whether you are a standard deduction filer or an itemizer because OBBBA impacts both!

Deductions Are Shifting — Again

For the majority of households filing income tax returns, the standard deduction has been high enough in recent years that itemizing didn’t make sense. But as thresholds and rules evolve, it may be worth revisiting that assumption.

Standard deductions were increased (a touch) again for single and married filers and will be inflation adjusted moving forward. For tax year 2025, the standard deduction is $15,750 for single filings / $31,500 married filing jointly filings.

For itemizers, though, OBBBA touched on nearly all categories of itemized deductions:

Mortgage Interest and now mortgage insurance premiums are deductible starting 2026.

State and Local Tax (SALT) deductions were previously limited to $10k, but that cap was raised by OBBBA to $40k starting in tax year 2025. This could impact many in the DMV!

Charitable deductions will see a new floor starting in 2026 that only contributions over 0.5% of AGI will be eligible to deduct.

Miscellaneous itemized deductions that were previously temporarily deleted by the Tax Cuts & Jobs Act in 2017 are not permanently deleted.

New “Below-the-Line” Opportunities

Several new “below the line” deductions are now available as well – they have restrictions, thresholds, and particulars, so work with your financial professional and tax advisor to learn more:

Senior deduction – available to standard and itemized filers

Tip income

Overtime income

Qualified auto loan interest

Charitable giving for standard filers – this one is pretty special as charitable giving deductions were previously limited to itemizers only. Now standard filers have an opportunity to get a tax break on their tax deduction.

What Matters Most Within the DMV

Here in the DMV, it’s generally a high-income demographic with high home ownership. I think 1) the increase to the SALT cap could single-handedly move some standard filers back to the itemizer track in this area with a much larger deduction than you expected. And 2) for standard filers, this new charitable deduction is really attractive – and just in time for Spring2ACTion!

What Do I Do with My Refund?

If these changes resulted in a large tax refund that you weren’t expecting, let’s talk about your situation and how to make best use of those newfound funds in your life.

Got questions on how the tax changes can impact your personal financial plan? Reach out to me lobrien@xmlfg.com so we can discuss further.

This communication is for informational and educational purposes only. No content or reference is intended to be a recommendation for the sale or investment in any product, strategy or service nor should it be perceived as individual advice. Please seek the advice of a financial advisor regarding your particular financial situation. XML Financial Group and its Wealth Advisors are not licensed tax or legal professionals. These materials are not intended to be used, and cannot be used by any taxpayer, for the purpose of avoiding penalties that may be imposed on the taxpayer under U.S. federal tax laws. Individuals should consult their personal tax or legal professional regarding tax filings, such that may be required for certain trusts, retirement and ERISA plans, and any tax- or legal-related investment decisions. Visit xmlfg.com for more information.

SEE ALSO: How High Earners Use a Backdoor Roth IRA—and Whether It’s Right for You