Document Retention Reminders!

Keeping records may not be glamorous, but trust us—future you will be very thankful. ✨

According to the American Institute of Certified Public Accountants (AICPA), businesses should maintain organized document retention policies to protect financial records, support audits, and stay compliant. Translation? Don’t toss those receipts just because your desk drawer is overflowing.

A good rule of thumb:

Tax returns & supporting documents → keep for at least 7 years

Payroll records → typically 4 years minimum

Bank statements & reconciliations → around 7 years

Permanent records (formation documents, major contracts, ownership records) → forever, babe ♾️

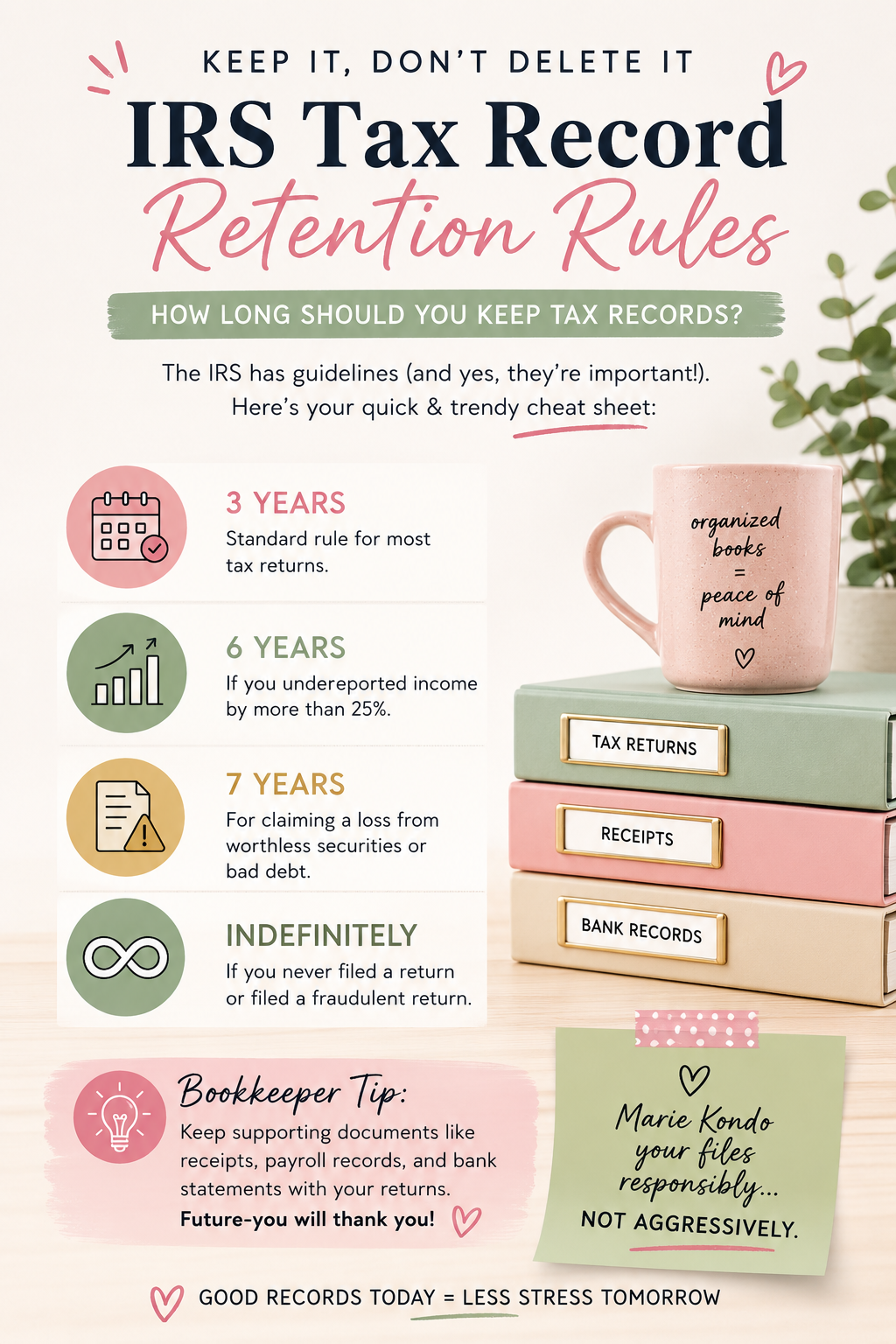

The Internal Revenue Service generally recommends keeping tax records for at least 3 years from the date you filed your return. However, there are a few important exceptions:

3 years → standard rule for most tax returns

6 years → if you underreported income by more than 25%

7 years → for claiming a loss from worthless securities or bad debt

Indefinitely → if you never filed a return or filed a fraudulent return

For businesses, it’s also smart to keep supporting documents such as receipts, payroll records, and bank statements organized alongside your returns in case questions ever pop up later.

Basically: Marie Kondo your files responsibly… not aggressively. ✨

The key is consistency. Whether you’re team color-coded filing cabinet or team “everything lives in the cloud,” having a retention system saves time, reduces stress, and keeps your business audit-ready.

Bookkeeper tip: If your file naming system currently looks like “FINAL_final_v2_USETHISONE.pdf,” it may be time for a refresh. 😉

Because organized books aren’t just pretty—they’re powerful.

SEE ALSO: Spring into Summer Sale at The Hive